A Ceasefire Dividend and a Data Reality Check: Week of May 26–30, 2026

Iran ceasefire signals pushed oil from $112 to $92 and Treasury yields lower for four straight sessions — but PCE hit a three-year high at 3.8%, GDP was revised down to 1.6%, the RBNZ held by a casting vote with explicit hike guidance, and the SARB became the first major EM bank to hike since the war began. The week closes with a packed June calendar led by the US May jobs report on June 6 and the ECB's June 11 decision.

Two questions defined last week: could Iran peace signals last long enough to reverse the oil shock that has been feeding global inflation? And would the data arriving Thursday — US PCE and the GDP revision — give the Fed's new Chair any breathing room? The answers were mixed. Oil retreated sharply but the ceasefire remains provisional; PCE hit a three-year high and GDP was revised down. Meanwhile, every major central bank with a decision before it leaned hawkish, and a packed June calendar opens with the question already posed: can a decelerating economy and persistent inflation coexist without forcing the Fed's hand?

Central bank scorecard

| Bank | Current rate | This week's decision | Next meeting |

|---|---|---|---|

| Fed | 3.50–3.75% | No meeting | June 16–17 (Warsh's first) |

| ECB | 2.15% | No meeting; April minutes released | June 11 |

| BoJ | 0.75% | No meeting | June (date TBC) |

| BoE | 3.75% | No meeting | June |

| RBA | 4.35% | No meeting (June pause confirmed) | June |

| RBNZ | 2.25% | Hold, 3–3 casting vote | July 8 |

| BoK | 2.50% | Hold (Gov. Shin's first meeting) | — |

| SARB | 7.00% | +25 bp hike (4–2 vote) | — |

| PBoC | 3.00%/3.50% LPR | No change (on hold 12+ months) | — |

The headline number for the week came not from a meeting but from a set of minutes. The ECB's April notes, released Thursday, confirmed that the hold at that meeting was a close call: several Governing Council members said they would not have objected to hiking outright had it been on the agenda.1 ING's chief economist called a June 25 bp move "almost a done deal" — "an insurance hike to demonstrate the bank's commitment to its inflation mandate."1 Eurozone flash CPI readings released Friday reinforced that framing: Germany's HICP eased to 2.6% in May (from 2.9%), but core ticked up to 2.5%, and Spain (3.6%), Italy (3.3%), and France (2.8%) held stubbornly elevated.2 Short-term inflation expectations in the bloc jumped to 4.0% in April (from 2.5%) even as five-year expectations stayed near 2.4%, giving the ECB cover to hike once without committing to a cycle.

The RBNZ decision was the week's most dramatic. Governor Anna Breman used her casting vote to break a 3–3 deadlock, keeping the official cash rate at 2.25% for a third consecutive meeting.3 The bank's statement warned that hikes would arrive "sooner and by more than previously expected" to counter the war-driven energy shock, and MPC member Gourley said rates were "likely to rise sooner rather than later."4 The decision reflects the same tension confronting several small open economies: energy-driven inflation that demands tightening, but demand already softening under the weight of higher fuel and transport costs.

The SARB had no such hesitation. Policymakers voted 4–2 to raise the repo rate by 25 bp to 7.0%, the first hike in three years.5 Governor Kganyago said the bank was prioritizing its 3% inflation target over a fragile domestic recovery — a move that effectively offset the government's $1 billion fuel subsidy package rolled out just weeks earlier.

Bank of Korea held at 2.50%, as expected. This was new Governor Shin Sung-hwan's first meeting; markets took the hold as a signal of continuity, with the focus remaining on how the global energy price trajectory affects Korea's import-heavy inflation profile.

Data watch: PCE hits a three-year high, GDP revised lower

The two most important US data prints of the week landed Thursday and pointed in uncomfortable directions simultaneously.

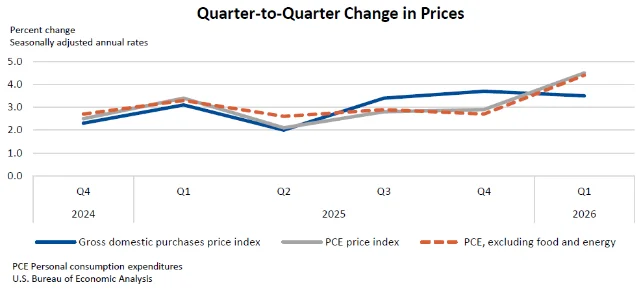

April PCE inflation came in exactly at consensus but at its highest level since May 2023: headline PCE rose to 3.8% year-on-year (from 3.5% in March) with a 0.4% monthly gain; core PCE (excluding food and energy) held at 3.3% y/y, up slightly from March, with a 0.2% monthly gain that was one-tenth below the 0.3% expected.7 The in-line print was enough to prevent a hawkish shock to markets — the dollar index briefly dipped after the release — but the absolute level, at nearly twice the 2% target, left no room for the Fed to stand down.

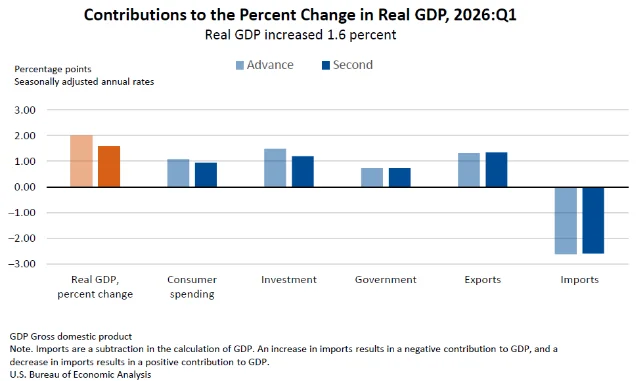

The GDP revision was the day's unwelcome companion. The BEA revised Q1 2026 real GDP growth to 1.6% annualized, down 0.4 pp from the 2.0% advance estimate.6 The downgrade was driven primarily by a larger-than-expected drag from private inventories (manufacturing and retail) and downward revisions to services spending, notably healthcare. Corporate profits grew by only $40.4 billion in Q1, against $246.9 billion in Q4 2025 — a sharp deceleration that Q4 figures had obscured.8 The combination — 3.8% PCE inflation running alongside 1.6% real growth — restores some stagflationary optics that policymakers have tried to avoid framing too directly.

The Fed's internal debate sharpened. Minneapolis Fed President Kashkari, who had opposed removing the easing bias in April, is now publicly saying inflation risks have overtaken labor-market downside risks.7 Governor Waller, who removed his easing bias in Frankfurt on May 22, said he would not hesitate to support hikes if inflation expectations show signs of de-anchoring. Fed funds futures on Friday priced roughly a coin-flip probability of at least one hike by year-end, with Chair Warsh's June 16–17 debut now carrying outsized interpretive weight for markets.

Australia's CPI added a regional data point: the ABS monthly index rose to 4.2% y/y in April (from 4.6% in March), with a 0.4% monthly gain on an original basis (−0.1% seasonally adjusted).9 The trimmed mean came in at 3.4%, and housing held at 6.3%. The headline moderation confirmed the RBA's decision to pause in June — Westpac still sees the next hike arriving in August or September — but the persistence of trimmed mean well above target means the pause is contingent, not terminal.

Tokyo CPI for May gave the BoJ another mixed reading: the core index (excluding fresh food) slowed for a sixth consecutive month to 1.3% y/y, missing the 1.5% forecast, while the headline remained at 1.4%.10 Government energy subsidies continue to suppress the index. The Japan Times cited analyst consensus that the BoJ remains on track for a June 25 bp hike to 1.00%, with MNI noting the probability still embedded in pricing runs north of 80% when cumulative hike pricing through August is totaled.11

FX and rates: the ceasefire trade dominates

Treasury yields declined for four consecutive sessions as Iran ceasefire optimism built through the week, erasing the yield spike that had been driven by the earlier oil surge. The 10-year ended Friday at 4.441% (down from 4.572% on Monday's open), the 30-year at 4.982% (down from 5.028%), and the 2-year at 3.996%.12 The relief came despite the PCE print: markets appeared to price the in-line read as "no worse than expected," preserving the peace-deal bid. Note that the 30-year had briefly touched 5.19% on May 20; the week's close at ~4.98% represents a meaningful reversal, though it remains well above levels seen before the Iran war began.

On FX, the dollar index ended the week near 98.90, down 0.1% Friday on the ceasefire reports.12 EUR/USD edged to $1.1663 — broadly stable at elevated levels consistent with the ECB's hawkish pre-positioning versus a Fed that has not yet pulled the trigger. USD/JPY held at 159.26 through Friday, maintaining proximity to the 160 level that has drawn Ministry of Finance rhetoric about intervention risk; the yen found no catalyst to strengthen while the Tokyo CPI data disappointed and the BoJ is not yet in action.

The currency market standout for the week was the New Zealand dollar, which showed little net movement despite the razor-thin RBNZ hold — possibly reflecting that the casting-vote result, combined with explicit guidance for earlier-than-expected hikes, was a net hawkish message. The Australian dollar touched 0.7183 heading into the weekend, supported by the CPI moderation that validated the June RBA pause without signaling extended easing.

Cross-asset: S&P's ninth straight weekly gain, oil in retreat

The S&P 500 logged its ninth consecutive weekly gain — its longest run since December 2023 — closing Friday at 7,580.12, with the Dow at 51,032.65 and the Nasdaq at 26,972.62.12 All three major indexes posted monthly gains for May. The BlackRock Investment Institute noted that since the Iran conflict began, the S&P 500 is up 8%, with that gain occurring alongside a 43% rise in Brent and nearly 60 bp added to 10-year yields — an unusual configuration suggesting equities have been pricing a peace dividend even as rates push higher.

Brent settled at $92.05 on Friday, WTI at $87.36 — both down roughly 1.8% on the day as markets awaited formal confirmation of the US-Iran ceasefire extension.12 Brent's descent from the $112 peak during active hostilities to the low-$90s reflects a significant reduction in the geopolitical risk premium, though the ceasefire remains provisional: President Trump had not yet formally approved the deal as of Friday's close.

Gold rose 1.18% Friday to $4,545 per ounce (US gold futures +0.98% to $4,543.60), lifted by ceasefire optimism, though spot gold was still on course for a monthly decline.12 The dip from intra-conflict highs mirrors Brent's trajectory, both assets having served as Iran-war hedges that partially unwind as peace signals accumulate.

European equities posted more muted gains for the week. Germany's DAX eased 1.8% on the week (though up 14.8% year-to-date) and France's CAC40 fell 2.3% (up 13.1% YTD), partly because eurozone data continued to show slowing PMIs even as inflation stayed elevated.13 Japan's Nikkei added 0.4% on the week (up 18.5% YTD). Hang Seng closed at 25,182.39, up 0.7% on the day Friday.

Week-ahead calendar: June 2–6

June opens with the most data-dense week of the half-year — with the US jobs report on Friday providing the principal test of whether the Fed's hike debate gains urgency or softens.

| Day | Key event | Why it matters |

|---|---|---|

| Mon June 2 | Global manufacturing PMIs final (May); US ISM Manufacturing (May); ECB Consumer Expectations Survey | May flash ISM mfg came in at 48.5%, slightly below consensus — any downside confirms demand softening |

| Tue June 3 | Eurozone CPI flash (May) | Last major inflation update before the ECB's June 11 meeting; consensus sees headline above 3% |

| Wed June 4 | US ADP Employment Change (May); ISM Services PMI (May); Fed Beige Book; Australian Q1 GDP | ADP and Beige Book will set tone for NFP expectations; BoJ Governor Ueda speaks |

| Thu June 5 | US jobless claims; US Challenger layoffs; ECB Lagarde speaks; RBA Governor Bullock speaks | Lagarde speech key ahead of June 11; Bullock will be watched for language shift on August hike |

| Fri June 6 | US May Jobs Report (NFP, UE rate, avg hourly earnings); Canadian jobs (May); RBI policy (Jun) | Bloomberg consensus: ~90k NFP, 4.3% unemployment rate. Strong print = Fed hike probability jumps; weak print = stagflation anxiety |

Fed speakers are active Monday through Thursday before the pre-meeting blackout: Kashkari and Hammack on Tuesday, Barr and Logan on Wednesday, Barkin and Daly on Thursday.14 Any coordinated tightening message ahead of the blackout would clarify whether the coin-flip on a year-end hike flips.

On the ECB timeline: the May eurozone flash CPI on Tuesday (June 3) is the final major data point before the June 11 meeting. Given the April minutes and the Big Four CPI readings, a miss below 2.8% consensus on Tuesday could give the doves a last-minute argument, but ING and markets currently treat the June hike as essentially locked in.1

The Iran deal status also remains in play. The ceasefire extension being discussed as of Friday would reopen Strait of Hormuz shipping for 60 days — enough, if approved, to push Brent further toward the $80s and meaningfully ease inflationary pressure heading into the July policy window.

Global Macro Weekly is an analytical digest. Nothing in this article constitutes investment advice. All data points are sourced from newswires, official statistical agencies, and central bank publications as cited.

Fuentes de referencia

- 1ING Think: ECB April minutes confirm hawkish bias

- 2Euronews: ECB rate hike in focus as Eurozone's 'Big Four' report stubbornly high inflation

- 3WSJ: New Zealand's central bank narrowly votes to hold rates

- 4Reuters: NZ central bank watching how much weaker demand would offset price increases

- 5Yahoo Finance/Semafor: South Africa hikes key interest rate

- 6BEA: GDP Second Estimate and Corporate Profits, Q1 2026

- 7FXStreet: Core PCE inflation rises to 3.3% in April

- 8WSJ: US GDP growth revised lower for first quarter

- 9ABS: CPI rose 4.2% in the year to April 2026

- 10Reuters: Core inflation in Tokyo stays below BOJ goal

- 11Financial Post: Tokyo inflation slowdown unlikely to derail BOJ rate hike

- 12Reuters: Wall Street ends higher, crude prices ease on potential US-Iran truce extension

- 13Kaohoon International: Market Roundup 28 May 2026

- 14Bloomberg/Yahoo Finance: Bond trader bets on Fed hike

Añade más opiniones o contexto en torno a este contenido.