Five-carrier monthly rate comparison

Side-by-side full-coverage quotes, May 26, 2026 (Insurify)

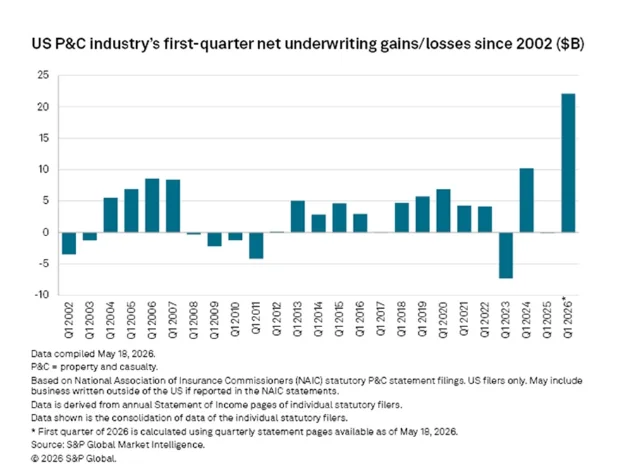

Three publicly documented Reddit switch cases from May 19–27, 2026 show real drivers cutting $720 to $1,800 per year without reducing coverage — set against a Q1 2026 rate climate where the industry posted its best underwriting result in 25 years and none of the six major carriers filed rate changes. Includes the four-step pre-flight checklist, life-stage quoting benchmarks from Insurify and NerdWallet May 2026 data, the retention-department gambit, and three anti-patterns (UM/UIM drop in Florida with $10K+ consequence, mid-claim switching, and post-bind underwriting demands).

| USAA (old) | State Farm (new) | |

|---|---|---|

| Monthly premium | $210 | ~$85 |

| Annual premium | ~$2,520 | ~$1,020 |

| Annual savings | ~$1,500 |

| Progressive (old) | National General (new) | |

|---|---|---|

| Monthly premium | $196 | $136 |

| Annual premium | ~$2,352 | ~$1,632 |

| Annual savings | $720 |

| Geico auto + Farmers home (old) | Allstate bundle (new) | |

|---|---|---|

| Combined annual (estimated) | Not disclosed individually | Saves ~$1,800/year vs. current |

| Annual savings | ~$1,800 |

이 콘텐츠를 둘러싼 관점이나 맥락을 계속 보강해 보세요.